Oil prices have surged in recent weeks as the rhetoric from US President Donald Trump regarding Iran has intensified and the threat of sanctions increased. Iran is one of the largest global oil producing nation and, should sanctions be imposed on 12 May, global supplies would tighten dramatically.

Oil prices have surged in recent weeks as the rhetoric from US President Donald Trump regarding Iran has intensified and the threat of sanctions increased. Iran is one of the largest global oil producing nation and, should sanctions be imposed on 12 May, global supplies would tighten dramatically.

Oil prices have already been rising on the back of the announcement last year from the 14 Opec nations to restrict output. In November they decided to extend those cuts until the end of this year.

Since the oil price is a key determinant in the pricing of Naphtha, which is then cracked to produce Ethylene and Propylene feedstock, historically there has always been a strong link between oil prices and polymer prices. And polymer producers have often cited the rising costs of oil as a justification for seeking price increases. The news of a surge in the oil price is therefore likely to be of concern for plastics processors, particularly for polyolefin products.

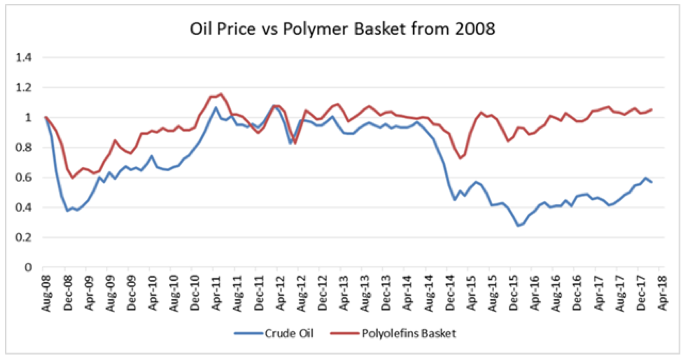

However, as we can see on the graph below taken from our monthly Price Know How publication, this causal link does not always hold.

The graph shows the relative value of the oil price versus a basket of polyolefins, taking pre-financial crisis data in 2008 as the reference point.

Whilst the trend is clearly similar, with the direction of the oil price typically being followed by a movement in polymer prices, this is not always the case and the differential between the oil price and polymer prices can vary significantly.

In the period from 2011 until the middle of 2014, during a period of excess supply, the differential between the movement in the oil price and polymer price was negligible, and the movement in the oil price and polymer price was very similar. However, during the period of supply shortages from 2015 onwards, the differential increased markedly showing that dramatic changes in the oil price did not pass through to polymer prices. This indicates a period of strengthening margins achieved by the feedstock and polymer producers.

So, whilst the oil price is an important factor in determining the polymer price trend, it is important to recognise that the prices of feedstocks and polymers are set by the market dynamics for those products themselves. Exchange rates, critically between the Euro and Dollar, are also of central importance.

And so, what are the expectations for polymer pricing given this latest upsurge?

In our opinion the oil price is unlikely to be a key determinant in the short to medium term. If we consider the capacity expansions in the US for both feedstock and polymers based on Shale gas, the market dynamics are likely to be dominated by surplus supply. And it is these dynamics which will likely determine polymer prices.

Whilst in the short term the firm oil price is likely to keep the pressure on both feedstock and polymer prices, this is likely to be short lived. The oil price will always remain a key variable to be observed by those looking to better understand the polymer market, however on this occasion the announcements should not leave polymer processors quaking in their proverbial boots.

If you would like to know more about the trends affecting feedstock prices and polymer prices we are running a free course in June called: ‘Understanding the Economics of the Polymer Supply Chain’.

Please contact Duncan Scott on 01530 560560 if you would like more details.